Is San Diego Still a Safe Haven for Multifamily Investors? 2025 Year-End Review

An honest look at cap rates, rent growth, and the real opportunities I'm seeing on the ground as we head into 2026.

By Nick Hernandez ·

If 2024 was the year of “wait-and-see,” 2025 has been the year of stabilization.

As we close out the fourth quarter, San Diego continues to prove its resilience. We aren’t seeing the explosive rent growth of the post-pandemic boom, but crucially, we aren’t seeing the distress prevalent in overbuilt Sun Belt markets like Austin or Phoenix.

San Diego remains a high-barrier-to-entry market defined by constraints. Here is my analysis of the multifamily sector using the latest Q3/Q4 2025 data and why I believe it remains a safe harbor for 2026.

Executive Summary: Year-End 2025 Snapshot

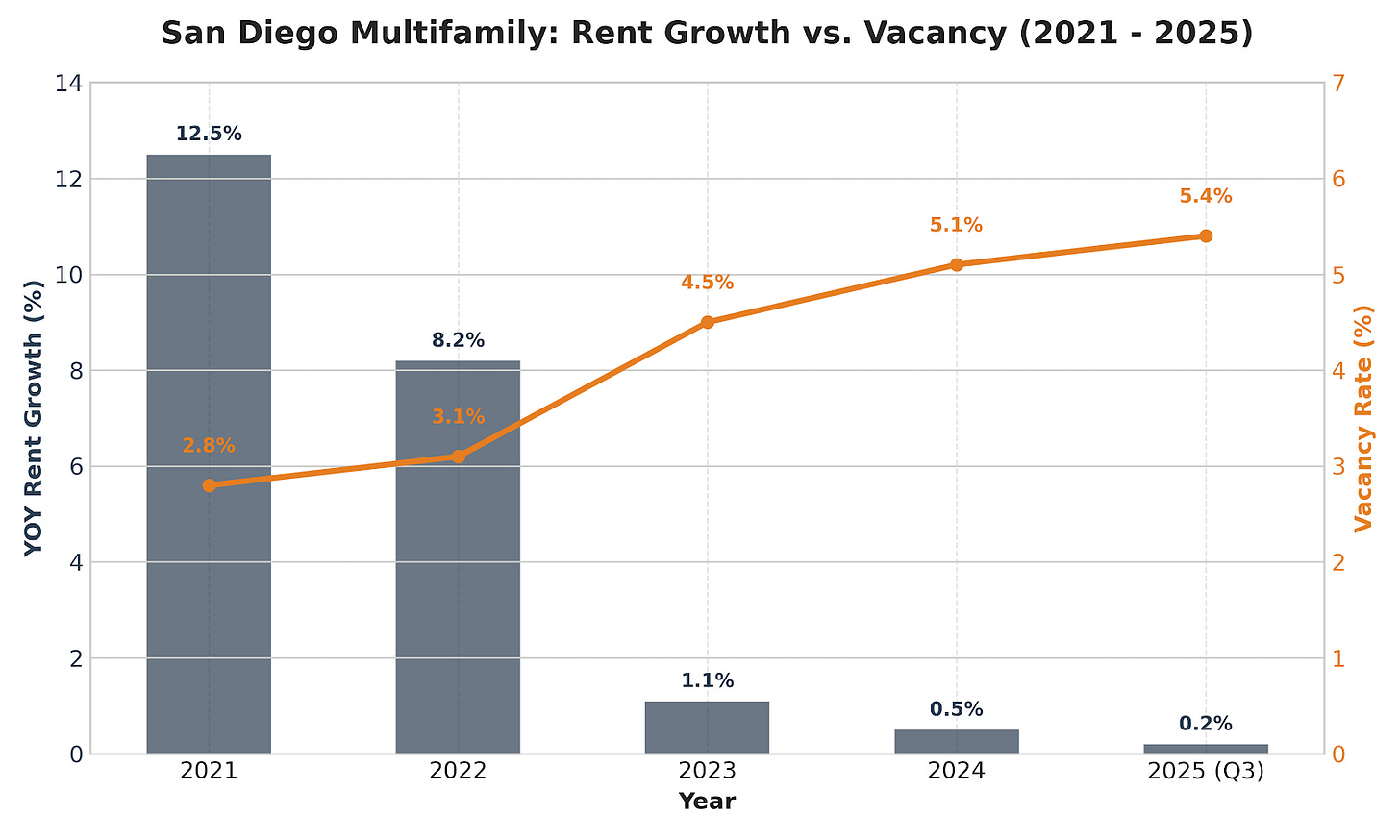

Vacancy Remains Manageable: The metro vacancy rate is hovering around 5.4%. While this is a slight uptick from the historic lows of 2022, it remains healthy compared to the national average.

Rent Growth Has “Flattened”: We are seeing virtually flat year-over-year rent growth of 0.2%. The days of double-digit spikes are gone; we are in a period of normalization where tenant affordability is the ceiling.

Transaction Volume is Mixed: Q3 2025 saw approximately $575 million in transaction volume. While this is a pullback from Q2, it signals that deals are getting done, albeit with more scrutiny on underwriting.

Construction Pipeline is Active but Peaking: With roughly 9,400 units currently under construction, we are working through a supply wave, but high construction costs have curbed future starts, meaning this new supply will taper off significantly by late 2026.

The Fundamentals: Vacancy and Rent Trends

While national headlines might talk about softening demand, San Diego is structurally different. Our geography and local politics severely limit how many new units can be built, creating a permanent floor for occupancy.

In late 2025, average asking rents in San Diego county stabilized at approximately $2,500 per unit, a marginal 0.2% increase year-over-year.

My take from the field: Based on the rent rolls I’m reviewing for clients right now, we are seeing the strongest retention in Class B assets in walkable submarkets like North Park and Hillcrest. However, owners pushing for aggressive rent bumps are facing pushback. The strategy right now is occupancy over growth.

Vacancy has settled at 5.4%. This slight softening is largely due to new deliveries in Mission Valley and Downtown. Concessions have returned for lease-ups in those Class A buildings, but the Class B market remains tighter.

The Investment Market: Sales and Cap Rates

The transaction paralysis is thawing, but pricing power has shifted.

We are currently seeing market cap rates for stabilized Class B product expand to the 4.7% – 5.7% range.

Who is selling? Owners with maturing debt who don’t want to refinance at current rates, or merchant builders looking to recycle capital.

Who is buying? Private capital and family offices remain the most active players in the sub-$20M space. They are looking for safety and tax benefits rather than immediate cash flow.

The “bid-ask” gap is closing, but it’s closing because sellers are finally accepting 2025 pricing. If you are a buyer, you have more leverage today than you’ve had in five years.

The “Moat”: Why San Diego Remains Safe

If you are worried about a recession in 2026, San Diego has a built-in defense mechanism: a severe housing shortage. This is the “moat” around your investment.

While approximately 4,600 units were delivered over the last 12 months, this barely scratches the surface of the Regional Housing Needs Assessment (RHNA) goals.

More importantly, the pipeline for 2027 is shrinking. The high interest rates for construction loans over the past two years caused many developers to pause projects.

What this means for you: With employment in the region’s key sectors remaining robust, the lack of significant future housing supply guarantees high occupancy rates for existing assets for the foreseeable future.

The 2026 Outlook: How to Play the New Year

The “easy money” era is over. 2026 will be about operational excellence.

A Return to True “Value-Add”: You can no longer rely on market momentum to lift your NOI. 2026 will be the year where strategic renovations (ADUs, high-ROI interior upgrades) are the only way to force appreciation.

Debt Market Clarity: Interest rates appear to have settled. This stability is giving investors the confidence to jump off the sidelines.

Submarket Bifurcation: Watch for a wider performance gap between highly walkable, amenity-rich neighborhoods and car-dependent outer suburban areas.

Final Thoughts

Is San Diego still a safe haven? Yes.

It may not offer the highest initial yield compared to the markets like the Midwest, but its combination of lifestyle appeal and restricted supply provides a safety net few other markets can match.

If you are reviewing your portfolio at year-end and trying to determine if you should hold, refinance, or exchange into a different asset type in 2026, let’s run the numbers together.

Book a call today